The “One Big Beautiful Bill” and Financial Planning

The “One Big Beautiful Bill” and Financial Planning

Preferred Resource Group | August 15, 2025

As you have likely seen, President Trump signed the major new tax and spending bill into law after Congress approved it. This is a comprehensive tax and spending bill, with over 900 pages, and makes significant changes to the tax code.

On an individual level, taxes are a central part of financial planning, and the provisions in this tax bill have immediate implications for household finances. From a financial market and economic perspective, many investors also worry about the level of government spending, the growing national debt, and other factors that have weighed on markets over the past two decades.

Thus, there are many angles from which to view the recently passed budget. This topic can also be politically controversial, so it’s important to focus on what matters. I’d like to summarize the key developments for you.

A Summary of What's in the New Tax Bill

The new law, which the administration calls the "One Big Beautiful Bill," extends and expands many provisions from the 2017 Tax Cuts and Jobs Act (TCJA) that were set to expire. Here are some key changes:

Tax Rates and Deductions:

Current tax rates and brackets set by the TCJA are now permanent, providing long-term certainty. Previously they were set to expire at the end of this year.

The standard deduction increases to $15,750 for single filers and $31,500 for married couples filing jointly.

The cap on state and local tax deductions increases significantly from $10,000 to $40,000. This limit will grow by 1% annually through 2029, then return to $10,000 in 2030.

Seniors get an additional $6,000 deduction (with income limits) through 2028. This is often referred to as the “senior bonus.”

The child tax credit increases from $2,000 to $2,200 per child, with future inflation adjustments.

Other Notable Changes:

Workers earning less than $150,000 can deduct up to $25,000 in tip income through 2028.

The alternative minimum tax exemption becomes permanent with higher thresholds.

Some green energy tax credits are eliminated.

Estate tax exemptions will remain high, increasing to $15 million for individuals and $30 million for couples in 2026.

Why This Matters for Your Financial Planning

This legislation removes what many called the "tax cliff" - a situation where tax rates could have increased dramatically if the previous provisions had expired. By providing certainty, it allows us to make more confident long-term financial plans for you and your family.

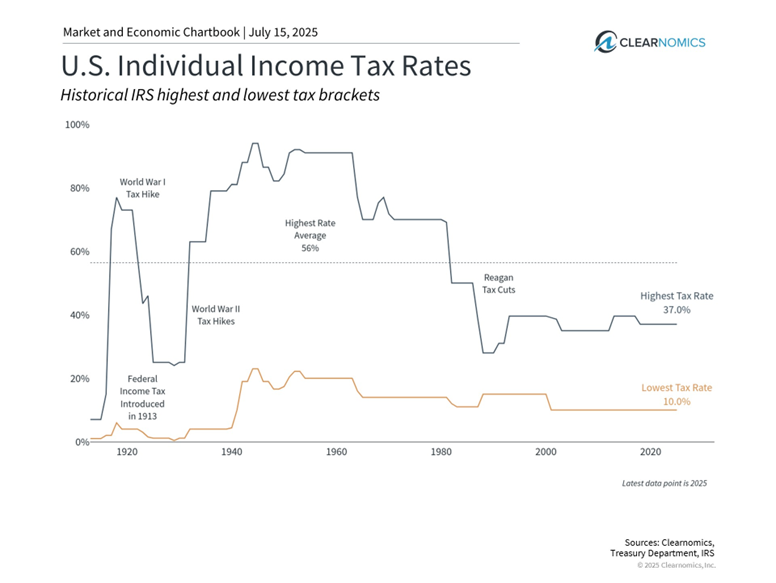

The bill maintains the relatively low tax environment we've experienced in recent decades. When you look at history, current tax rates remain well below the peaks of the 20th century, when top rates sometimes exceeded 90% during wartime periods.

For estate planning, the higher exemption limits mean fewer families will be subject to federal estate taxes. However, it's still important to have a comprehensive plan for passing assets to future generations, especially since some states have their own estate taxes with lower thresholds.

The Bigger Picture: Government Spending and Debt

While the tax changes are positive for many families, they do come with broader economic considerations. The Congressional Budget Office estimates this bill will add over $3 trillion to the national debt over the next decade. The federal debt already totals $36.2 trillion, or around $106,000 per American.

This situation isn't new - government borrowing has increased consistently over decades. To put this in perspective, the last balanced federal budgets occurred 25 years ago. This is because most government spending goes to programs like Social Security, Medicare, defense, and interest payments on existing debt, which are politically difficult to reduce.

From an investment standpoint, higher debt levels can influence interest rates and inflation over time. However, many of the worst-case scenarios that investors worry about haven't materialized. The key is maintaining a diversified portfolio that can perform well across different economic environments.

What This Means for Your Investment Strategy & Moving Forward

While tax policy changes can affect your personal financial situation, they typically have a limited impact on long-term investment opportunities. Markets have historically grown regardless of tax policy changes, and the economy has shown resilience across different fiscal environments.

The key takeaway is that this bill extends the current low-tax environment and provides more certainty for planning. While there are broader concerns about government debt, this shouldn’t impact your investment approach. A well-constructed, diversified portfolio aiming to weather various economic conditions remains a time-tested strategy toward building wealth over time.

We'll continue monitoring how these changes develop and their impact on your financial plan. As always, please don't hesitate to reach out with any questions.

Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual.

All investing involves risk including loss of principal. No strategy assures success or protects against loss. There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk.

The economic forecasts set forth in this material may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Sources

https://app.clearnomics.com/commentaries/56529

Copyright (c) 2025 Clearnomics, Inc. All rights reserved. The information contained herein has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice. All reports posted on or via www.clearnomics.com or any affiliated websites, applications, or services are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings may be mentioned occasionally, but should not be construed as a recommendation to buy, sell, or hold the company's stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security--including mutual funds, futures contracts, and exchange traded funds, or any similar instruments. The text, images, and other materials contained or displayed in this report are proprietary to Clearnomics, Inc. and constitute valuable intellectual property. All unauthorized reproduction or other use of material from Clearnomics, Inc. shall be deemed willful infringement(s) of this copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Clearnomics, Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Clearnomics, Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.